By Jay Shareef and Chris Rhoads

Long-term care costs should be an important factor when planning for retirement. Research suggests that most Americans turning 65 this year will need at least some form of long-term care as they age—and long-term care is expensive.

Of course, the cost of long-term care depends on the type of care needed and the location in which long-term care services are received. According to the Genworth Cost of Care Survey, the national median costs of long-term care range from around $1,690 per month for adult day care services to around $9,034 per month for a private room in a nursing home.

Cost of Long-Term Care in Maryland

The following data shows average costs based on facilities all over Maryland, but the actual costs of care may vary in your specific location. Additionally, some long-term care needs can be fulfilled by family and friends, so depending on the support group of the person needing care, these costs may not be necessary for all retirees.

On the other hand, some old-age illnesses such as Alzheimer’s will almost always result in the need for long-term care during the late stages of the disease, despite how supportive or available loved ones are to help.

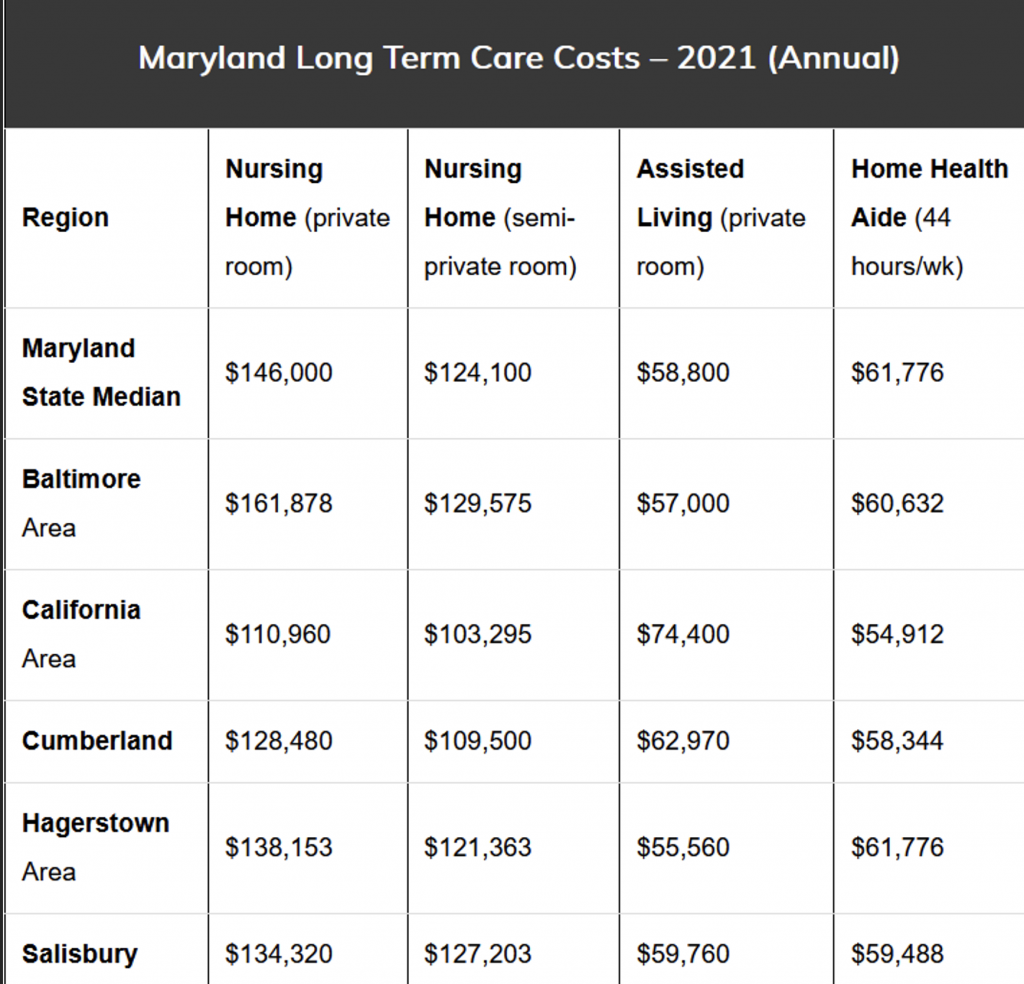

No matter what, it’s worth considering the need for long-term care costs as part of your retirement plan. The following table shows the median cost of long-term care services in Maryland:

As you can see, long-term care expenses are significant. Nursing home care, whether in a semi-private room or private room, may be well above most people’s monthly mortgage payments.

So how can you build these expenses into your retirement plan if you had planned on mitigating housing costs in the remaining years of your life?

Options to Pay for Long-Term Care

If thinking about paying for these costs on your own feels overwhelming, you have options. The three most common options include:

- A stand-alone long-term care insurance policy

- Addition of a long-term care rider to a life insurance policy

- Long-term care add-on to a fixed or indexed annuity

Stand-alone policies have been decreasing in popularity because the annual premiums can be quite expensive and the policies usually offer no cash benefit to survivors if the benefits aren’t used. However, stand-alone policies may be a good option for those who can afford the premiums and are relatively sure they’ll need long-term care coverage later in life.

Two better options might be to add long-term care insurance to existing contracts you own. If you have a permanent life insurance policy, many insurers offer an add-on called a long-term care rider. For an additional premium, the rider may come with death benefits.

And if you own an annuity, you may be able to purchase a similar add-on in which additional amounts would be added to your monthly annuity income if you ever need to pay for long-term care.

Partner With an Expert to Make the Right Decision

No one can predict the future, but long-term care expenses are a very real possibility you may have to contend with. You have a lot of options in front of you, so we don’t blame you if you’re feeling overwhelmed. Everyone’s situation is different, and a variety of factors should determine how you build long-term care considerations into your retirement plan.

Instead of making this decision alone, partner with trusted experts like the team at WealthFlow Financial. We can help you understand your options and make the smartest decision for you and your family.

If you don’t already have an advisor helping you do that, reach out to us at (301) 798-5250 or schedule a phone call now.

About Jay

Jay Shareef is vice president, financial advisor, federal benefits consultant, and co-founder at WealthFlow Financial. As a U.S. Army veteran, Jay is passionate about helping federal employees create a bulletproof plan for retirement and navigate the often confusing and complicated federal benefits landscape. He spends his days educating and providing clients with unbiased insurance benefits and retirement strategies to help his clients create guaranteed income for life. As a problem-solver and trustworthy resource, Jay always puts his clients and their needs first so they can find financial peace of mind. To learn more about Jay, connect with him on LinkedIn.

About Chris

Chris Rhoads is a co-founder and vice president of WealthFlow Financial. As a registered investment advisor and independent financial professional, Chris is committed to helping his clients in retirement and he takes a holistic approach to financial planning that includes insurance and risk management, investments and wealth management, retirement income planning, and estate and tax planning. Chris has been married to his wife, Tia, since 2009 and they live in Frederick, MD, together with their two young daughters. In his free time, Chris enjoys traveling, watching sports, and being active in causes about which he cares passionately. To learn more about Chris, connect with him on LinkedIn.